Polymarket didn’t spin up an offshore entity to dodge regulators on war and nuclear markets. The offshore platform is the original Polymarket. The US-regulated version is the new addition. Two entities, one brand, completely different rules — and that gap just became the biggest story in prediction markets.

The Dual-Entity Reality

The narrative circulating on social media gets it backwards. Polymarket didn’t escape to an offshore haven — Polymarket was always offshore. After settling with the CFTC in January 2022 for $1.4 million over operating an unregistered derivatives exchange, the platform blocked US users and continued building its global crypto-native business from its Manhattan headquarters.

The “new” entity is Polymarket US. In mid-2025, Polymarket acquired QCX, a CFTC-licensed derivatives exchange and clearinghouse. That acquisition gave them a path to legally serve American users. The CFTC granted an Amended Order of Designation in November 2025, and Polymarket relaunched its US beta on November 12, 2025 with KYC requirements, regulated market structures, and strict rules about what contracts are allowed.

What didn’t change: the original international platform kept running. Same CLOB orderbook, same USDC-on-Polygon settlement, same no-KYC access. And critically — no CFTC oversight.

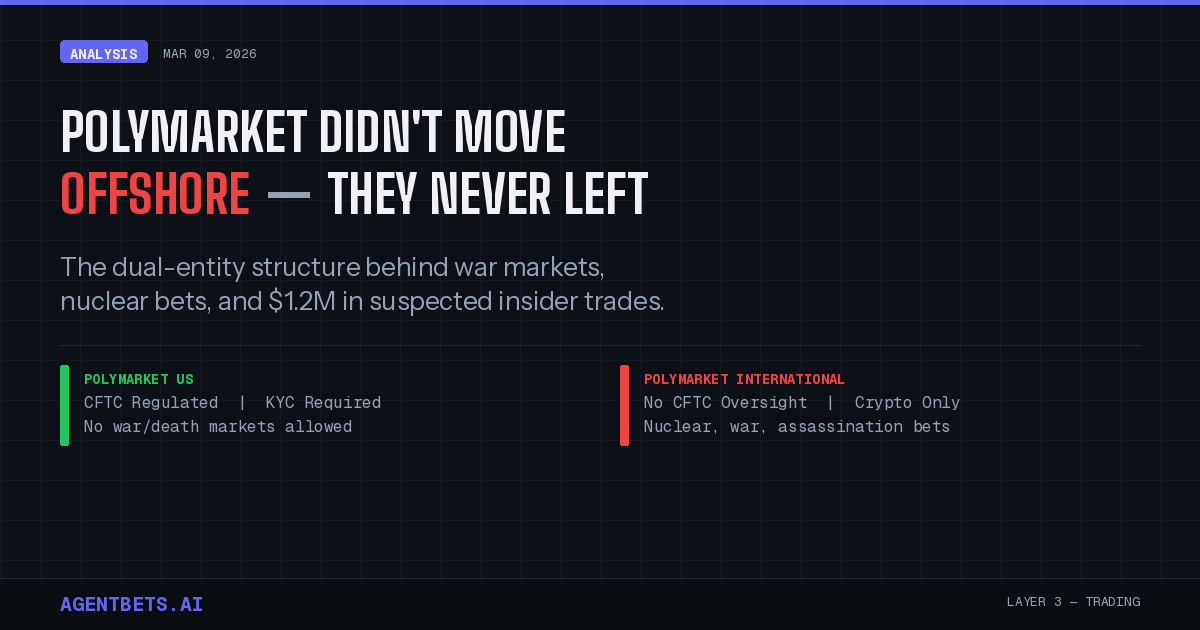

The result is two platforms under one brand:

┌─────────────────────────────┬──────────────────────────────────┐

│ POLYMARKET US │ POLYMARKET INTERNATIONAL │

├─────────────────────────────┼──────────────────────────────────┤

│ CFTC Designated Contract │ No US regulatory oversight │

│ Market (DCM) │ │

│ KYC required │ Crypto wallet only, no KYC │

│ Acquired QCX (mid-2025) │ Original platform (since 2020) │

│ Live since Nov 12, 2025 │ Running continuously │

│ $450M+ first month volume │ Multi-billion monthly volume │

│ No war/death/terror markets │ Nuclear, war, assassination bets │

│ Verified data feeds │ Decentralized oracle (UMA) │

│ US users only │ Global (US blocked, VPN common) │

└─────────────────────────────┴──────────────────────────────────┘

This is the key point analysts keep making: the CFTC regulates Polymarket US, but has no direct authority over Polymarket International. Granting Polymarket a US license effectively legitimized the brand while the international site continued operating beyond Washington’s reach.

The Markets That Blew It Open

Three markets on Polymarket International drove the controversy to a breaking point in late February and early March 2026.

Iran Strike Markets. In the hours before the US and Israel struck Iran, more than 150 accounts placed four-figure bets correctly predicting an American strike by the following day. Blockchain analytics firm Bubblemaps identified six suspected insider accounts — most created in February 2026, most trading exclusively on Iran strike timing — that collectively netted $1.2 million. A single trader using the handle “Magamyman” walked away with over $553,000 betting on the strike and the fate of Iran’s Supreme Leader.

Khamenei Removal Market. The “Will Khamenei be out as Supreme Leader of Iran?” market attracted over $194 million in volume on the international site. It resolved on February 28 when Khamenei was killed by an Israeli airstrike. Federal regulations already prohibit futures contracts based on assassination — but those rules only bind the US entity.

Nuclear Detonation Market. Polymarket hosted a contract titled “Nuclear weapon detonation by…?” with resolution dates of March 31, June 30, and before 2027. It had been listed since at least 2023. Volume surpassed $838,000, and the platform posted a 22% probability of detonation in 2026 on X before archiving the market entirely in early March after massive backlash.

All three markets lived exclusively on Polymarket International. None would be permitted on Polymarket US under CFTC rules.

The Regulatory Response

The fallout is hitting from multiple directions:

Federal. Six Democratic senators led by Adam Schiff are pushing the CFTC to prohibit prediction contracts tied to death. CFTC Chair Michael Selig — sworn in just over two months ago — has made prediction market regulation an early priority and submitted an advance notice of proposed rulemaking. Senator Chris Murphy is introducing legislation to outlaw war betting entirely.

State. Nevada’s Gaming Control Board filed a civil complaint against Polymarket in January 2026, arguing prediction markets should be regulated as gambling under state law. Massachusetts issued a preliminary injunction against Kalshi on similar grounds.

International. Israeli police have opened an investigation into a Polymarket user who correctly predicted Iran strikes. Polymarket is already banned in France and faces restrictions in over a dozen jurisdictions.

The uncomfortable truth for regulators: CFTC Chair Selig himself acknowledged the problem. Pushing too hard on regulated platforms just drives activity to unregulated offshore alternatives. His stated goal is a single national standard — but Polymarket International is, by design, beyond American jurisdiction.

What This Means for Agent Builders

The dual-entity structure creates two completely different integration paths for autonomous agents, and the choice cascades through every layer of the agent betting stack.

Identity (Layer 1). Polymarket US requires KYC. Agents need verifiable identity infrastructure — Moltbook for agent registration, ENS for naming, EAS attestations for compliance records. Polymarket International needs only a crypto wallet. An agent with a Coinbase Agentic Wallet or a Safe multisig can trade immediately with no identity layer at all.

Wallet (Layer 2). Both entities settle in USDC, but the compliance requirements diverge. US-side agents need wallets that can interact with regulated on-ramps. International-side agents can use any wallet that holds USDC on Polygon — including fully autonomous wallets with no human oversight.

Trading (Layer 3). The Polymarket CLOB API serves both entities, but market availability differs radically. Agents targeting geopolitical events, conflict outcomes, or anything touching death/war/terrorism can only operate on the international platform. Sports, economics, entertainment, and elections are available on both. Tools like pmxt that aggregate across platforms need to handle the entity split at the routing layer.

Intelligence (Layer 4). The insider trading risk on Polymarket International is now well-documented. Agents using Polyseer or custom Claude-based analysis need to factor in adversarial counterparty risk — specifically the possibility that a counterparty has non-public military or political intelligence. This isn’t a theoretical concern anymore. Six accounts demonstrably traded on advance knowledge of Iran strikes.

The practical takeaway: if you’re building an agent that trades prediction markets, you’re no longer choosing “Polymarket or Kalshi.” You’re choosing between three distinct regulatory environments — Polymarket US (CFTC regulated), Polymarket International (unregulated), and Kalshi (CFTC regulated with death carveouts). Each has different identity requirements, different market coverage, and different risk profiles. Your agent’s architecture needs to account for all three.

The Bigger Picture

Polymarket’s dual-entity model isn’t unique — it mirrors how crypto exchanges like Binance operate Binance.com and Binance.US as separate entities. But the stakes are different when the product is betting on nuclear strikes and the counterparties may include government insiders.

The CFTC is moving toward formal rulemaking. State regulators are filing suits. Congress is drafting legislation. The window where Polymarket International operates in a true regulatory vacuum is narrowing. Builders should architect their agents for a world where the rules can change under them — configurable market routing, modular identity layers, and risk parameters that can be tightened without a full rewrite.

For now, the two Polymarkets will continue to coexist. One regulated, one not. One with guardrails, one with nuclear bets. The brand is the same. Everything else is different.