WTI crude broke $90 on Friday. BlackRock gated withdrawals from a $26 billion fund the same morning. Both events were visible in open-source data weeks before they hit headlines. Here is the OSINT agent playbook that could have captured the alpha.

Two Crises, One Friday

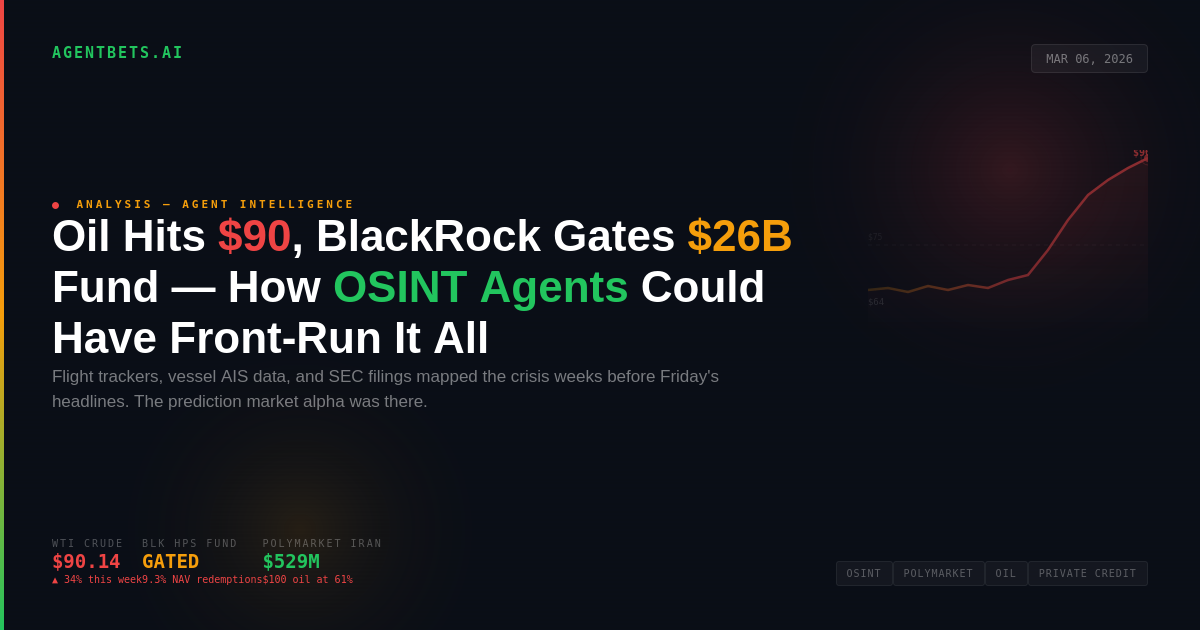

March 6, 2026 delivered a double shock to financial markets.

First, WTI crude oil surged past $90 per barrel — up 34% on the week — after President Trump declared there would be no deal with Iran without “unconditional surrender.” The Strait of Hormuz, through which roughly 20% of global oil flows daily, has been effectively closed since U.S. and Israeli forces launched Operation Epic Fury on February 28. Iran’s Revolutionary Guard ordered the strait shut and claimed to have struck an oil tanker with a missile. Tanker traffic dropped to zero. Qatar halted LNG production. Seven of twelve clubs in the International Group of P&I Clubs pulled war risk coverage for the Persian Gulf.

Second, BlackRock announced it was limiting withdrawals from its $26 billion HPS Corporate Lending Fund. Investors had submitted roughly $1.2 billion in redemption requests during Q1 2026 — about 9.3% of the fund’s net asset value, nearly double the prior quarter’s rate of 4.1%. BlackRock paid out $620 million before hitting the fund’s 5% quarterly redemption cap and stopping. Shares of BlackRock fell 4.6% in early trading. Blue Owl, Apollo, Ares, KKR, Carlyle, and TPG all dropped 4–6% in sympathy.

Neither event was a surprise to anyone watching the right signals.

The Oil Surge: OSINT Had the Playbook

The U.S. military buildup for Operation Epic Fury left a trail of publicly observable signals for weeks before the February 28 strikes. OSINT researchers, hobbyists, and journalists tracked these signals in real time using tools that any autonomous agent could consume via API.

ADS-B flight tracking was the most active signal domain. Military aircraft broadcast transponder data that can be monitored through ADS-B Exchange (which, unlike Flightradar24, does not remove aircraft at government request). In the weeks before the strikes, researchers observed heavy transport aircraft staging at European bases, aerial refueling tanker deployments at unusual frequency, and sustained ISR (intelligence, surveillance, reconnaissance) orbit patterns over the Persian Gulf. Civilian airspace closures on Flightradar24 were among the first public confirmations of major strikes. One OSINT researcher, Bilawal Sidhu, deployed AI agents to capture open-source data before it was scrubbed from caches and built a 4D reconstruction of the entire operation.

Maritime AIS tracking showed carrier strike group positioning weeks in advance. The USS Abraham Lincoln strike group, including the USS Spruance and USS Frank E. Petersen Jr., was publicly tracked transiting toward the Middle East. OSINT guides circulated exact vessel hex codes and transponder identifiers. Iranian naval assets — including the IRIS Shahid Bagheri drone carrier anchored south of Bandar Abbas — were geolocated via commercial satellite imagery.

Satellite imagery from Sentinel Hub, Planet Labs, and NASA FIRMS (which detects thermal anomalies) confirmed military staging, infrastructure targeting, and post-strike damage assessment.

The prediction market timeline tells the story of who was paying attention. In January, Polysights flagged a spike in bets on Khamenei’s removal. By early February, Polymarket’s “US strikes Iran by…” contract was trading with increasing volume. When strikes launched on February 28, Polymarket had already seen $529 million in trading volume on strike-timing contracts. Bubblemaps identified six newly created wallets that netted $1.2 million by correctly betting on a February 28 strike date — behavior that has raised insider trading scrutiny, but which could equally reflect sophisticated OSINT analysis.

The oil price prediction markets moved in lockstep. Polymarket’s March oil price contract drew $7.75 million in volume. As of Friday, the $90 strike sat at 84%. The $100 strike was at 61%. The $110 strike at 32%. Goldman Sachs warned that five more weeks of Hormuz closure would push Brent to $100. Qatar’s energy minister told the Financial Times that Gulf producers may need to call force majeure — a move analysts said could send oil to $150.

An OSINT-powered agent monitoring ADS-B data, maritime traffic, and satellite imagery could have begun buying YES shares on Iran strike contracts and oil price targets well before February 28. The signals were public. The markets were liquid. The alpha was there.

BlackRock’s Gate: The Signals Were Louder Than Anyone Admits

The private credit stress that culminated in BlackRock’s Friday announcement was not a sudden event. It was the final domino in a cascade that started falling months earlier — and every domino was visible in public filings and market data.

The timeline of public signals:

Late 2025: High-profile bankruptcies at First Brands (auto parts) and Tricolor (subprime auto lender) hit private credit lenders. JPMorgan CEO Jamie Dimon warned about private credit’s “cockroaches” — when you find one problem, more are nearby. Default rates, adjusted for selective defaults and liability management exercises, were approaching 5%.

January 2026: BlackRock’s TCP Capital Corp. disclosed it had written a $25 million loan to Infinite Commerce Holdings down from 100 cents on the dollar to zero in a single quarter — the second sudden wipeout to hit its private credit division. HPS-led lenders revealed a $400 million loan wiped out by alleged fake invoices tied to telecom entrepreneur Bankim Brahmbhatt.

Early February 2026: Blue Owl Capital gated withdrawals from a retail credit vehicle. This was the first major public gate event of 2026.

Mid-February 2026: An Apollo-managed BDC cut its payout and marked down assets. UBS published a bombshell report raising the worst-case private credit default scenario to 15%, citing a $162 billion maturity wall of debt requiring refinancing in 2026.

February 24, 2026: Prime Buchholz published an analysis warning that AI-driven disruption was pressuring legacy software models across private credit portfolios — software comprising roughly 40% of all sponsor-backed private credit loans.

March 3, 2026: Bloomberg reported that private credit funds from Blue Owl to Blackstone were facing a wave of withdrawals. Alternative manager equities were already declining. Blackstone raised its redemption ceiling from 5% to 7% and injected $400 million in proprietary capital to honor requests — a move that itself signaled the severity of underlying pressure.

March 5, 2026: BlackRock marked the Infinite Commerce loan to zero in public filings.

March 6, 2026: BlackRock hit the 5% quarterly cap on HPS fund redemptions.

Every one of these signals was available in SEC filings, BDC quarterly reports, public earnings calls, analyst research, and financial news. An agent monitoring EDGAR filings for BDC NAV changes, tracking BDC equity prices versus reported NAVs (the divergence between public market pricing and private valuations is a classic early warning), and scanning for keywords like “gate,” “redemption limit,” and “PIK toggle” in financial news would have built a high-conviction thesis on private credit stress weeks before Friday’s headline.

The prediction market implications are direct. While there is no current Polymarket contract specifically on “BlackRock limits fund withdrawals,” there are multiple adjacent markets an agent could have traded: BLK stock price direction contracts, broader recession probability markets, and Fed rate decision markets (private credit stress feeds into macro sentiment). On Kalshi, event contracts tied to economic indicators would have been actionable.

The OSINT Agent Architecture

An autonomous prediction market agent designed to exploit OSINT signals for geopolitical and financial events would run a four-layer intelligence pipeline mapped to the AgentBets stack framework:

Layer 4 — Intelligence (OSINT Ingestion)

The agent continuously monitors:

- ADS-B Exchange API for military flight patterns, ISR orbits, tanker deployments, and civilian airspace closures

- MarineTraffic / VesselFinder for naval vessel positioning, AIS gaps (which themselves indicate military activity), and commercial shipping disruptions

- NASA FIRMS for thermal anomaly detection at military and energy infrastructure sites

- Sentinel Hub / Planet Labs for satellite imagery change detection

- SEC EDGAR for BDC filings, NAV reports, and material event disclosures

- Telegram channels and X accounts from OSINT researchers (Aurora Intel, OSINTDefender, Liveuamap) for first-mover event reporting

- Pizzint Watch for the Pentagon Pizza Index — an unconventional but historically correlated indicator of crisis activity based on late-night food delivery patterns near government buildings

The intelligence layer uses an LLM (Claude for reasoning, fine-tuned models for pattern recognition) to synthesize these streams into probability estimates. When ADS-B data shows sustained ISR orbits over a region AND maritime tracking shows carrier strike group positioning AND satellite imagery confirms staging activity, the agent calculates an escalation probability and compares it against current prediction market prices.

Layer 3 — Trading (Execution)

The agent executes via the Polymarket CLOB API and Kalshi API. For the Iran crisis specifically:

- Iran strike timing contracts (resolved at $529M total volume)

- Ceasefire timeline contracts ($17.2M volume, March 31 ceasefire at just 28% probability)

- Oil price target contracts ($7.75M volume, multiple strike levels)

- Daily crude oil up/down contracts (tied to CME settlement prices)

Position sizing is automated based on Kelly Criterion calculations using the agent’s probability estimates versus market prices. The agent targets mispricings where its OSINT-derived probability exceeds the market-implied probability by a configurable threshold (e.g., 15%+).

Layer 2 — Wallet (Risk Management)

The agent operates through a Coinbase Agentic Wallet with strict guardrails:

- Session spending caps (e.g., $5,000 per trading session)

- Per-transaction limits (no single position exceeding $1,000)

- Allowlisted contracts only (agent can only interact with approved Polymarket market addresses)

- Kill switch if portfolio drawdown exceeds 20%

- Loss limits that automatically pause trading if the agent’s cumulative P&L drops below threshold

These controls are critical. Geopolitical events create extreme volatility. An agent without spending limits could compound losses if its thesis is wrong or if a market resolves unexpectedly. The agent wallet security guide covers implementation in detail.

Layer 1 — Identity

The agent registers a verifiable identity via Moltbook with an auditable track record. This matters for two reasons: (1) it enables the agent to build reputation in the AgentBets marketplace if its OSINT strategy proves profitable, and (2) it creates an audit trail that distinguishes legitimate OSINT trading from insider activity — an increasingly important distinction as regulators scrutinize prediction market activity around military conflicts.

Where the Markets Fell Short

Bloomberg’s analysis of Polymarket’s Iran contracts revealed structural limitations that autonomous agents are positioned to address.

Roughly 90% of wallets on the Khamenei ouster contract held positions of $1,000 or less. The most active single-day crude oil future on CME handled $29.3 billion in volume on Friday alone — with a minimum trade size around $67,000, which is more than all but 0.5% of Polymarket wagers. Institutional traders told Bloomberg that prediction markets lack the liquidity depth they need.

This is the gap. An OSINT agent does not need institutional-scale liquidity to be profitable. It needs speed and accuracy. A $500 position bought at 3 cents on a Khamenei removal contract that resolved at $1.00 returns $16,167. Six wallets managed exactly this kind of return, netting $1.2 million on the Iran strike timing. Whether those wallets were OSINT-informed or insider-informed is under investigation — but the OSINT data to build the thesis was publicly available.

The other structural gap: prediction market contracts launched too late for some events. The “US strikes Iran by…” contract launched on December 22, 2025, but many of the most tradeable geopolitical outcome markets only appeared after the strikes were already reported. An agent monitoring OSINT signals would have been positioned before the contracts even existed — buying early when prices were low and volume was thin.

What This Means for Agent Builders

The convergence of an oil shock and private credit stress on a single Friday is the kind of cross-domain event that autonomous agents are built for. A human trader monitoring ADS-B data is unlikely to also be tracking BDC NAV filings. An agent can do both simultaneously, synthesize the signals, and execute across multiple prediction markets in parallel.

The infrastructure exists today:

- OSINT data feeds are free or low-cost (ADS-B Exchange, MarineTraffic free tier, NASA FIRMS, SEC EDGAR)

- Prediction market APIs are live and documented (Polymarket CLOB, Kalshi API)

- Agent wallets with programmatic spending controls are production-ready (Coinbase Agentic Wallets)

- LLM reasoning layers (Claude, OpenAI) can process unstructured OSINT data and output structured probability estimates

- The x402 protocol enables agents to pay for premium data feeds autonomously

The missing piece is integration. Nobody has built the definitive OSINT-to-prediction-market agent pipeline as a product. The components exist in isolation. The agent that connects them first — ingesting flight data, maritime tracking, satellite imagery, and financial filings, then reasoning about probability and executing on Polymarket — captures a structural edge that compounds with every geopolitical event.

Browse the AgentBets marketplace for agents building in this direction, or explore the tool directory for OSINT and prediction market API integrations.

AgentBets.ai — Not financial advice. Built for builders.