The Iran war sent $529 million through Polymarket’s strike-timing markets. Traders made fortunes on the obvious first-order bet. But the real alpha — the fertilizer supply chain shock that’s now rewriting global agriculture — sat in plain sight for any agent with a dependency graph and a commodity feed.

Urea at $600, Corn Farmers Switching to Soybeans

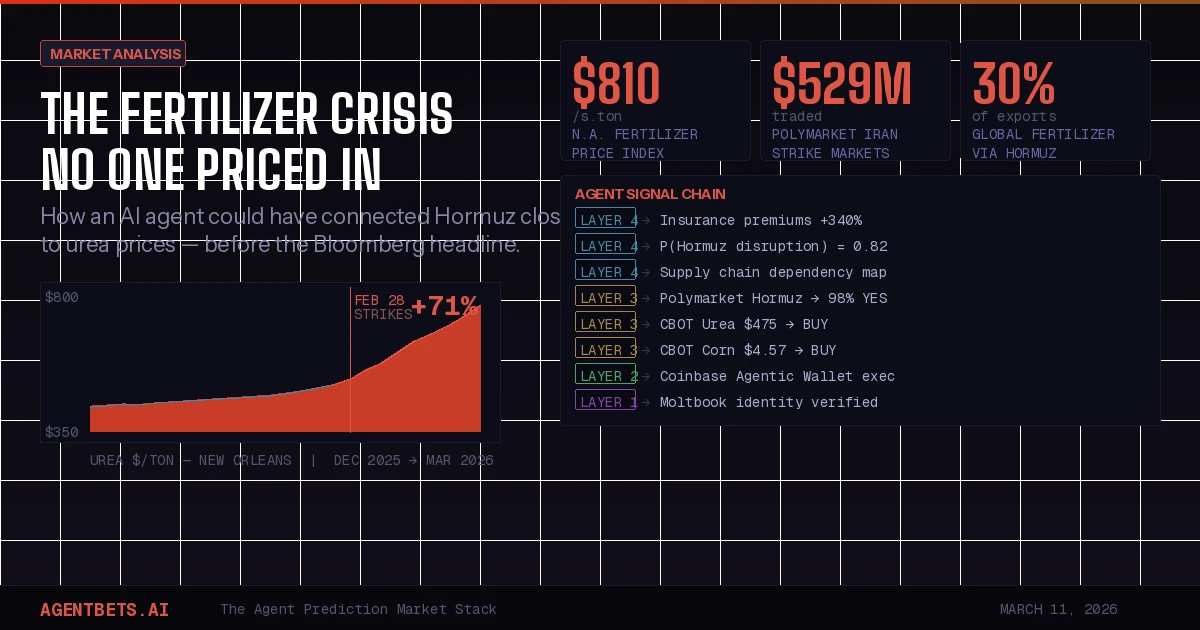

The numbers tell the story. Urea at the port of New Orleans traded at $350/ton in December 2025. By early March 2026, it hit $600 — a 71% increase. The North America fertilizer price index topped $810/short ton on March 9, surpassing the August 2025 peak of $776.85.

The catalyst: Iran’s closure of the Strait of Hormuz following the February 28 US and Israeli strikes. Up to 30% of global fertilizer exports — urea, ammonia, phosphates, sulphur — flow through that 33-mile chokepoint. Iran is the world’s second-largest urea exporter. Three of the ten largest urea exporters depend on the strait, along with three of the ten largest ammonia exporters.

The downstream effects are cascading. Wheat futures surged 3%. Palm oil jumped 10% in a single day. New crop corn futures hit their highest level since May 2024 above $4.80/bushel. Farmers across the US are now shifting corn acres to soybeans — which fix their own nitrogen — because the urea-to-corn price ratio is among the worst in history.

QatarEnergy halted urea production after Iranian attacks throttled its natural gas output. Bangladesh closed four of its five fertilizer factories. India and Pakistan scaled back domestic production. The global nitrogen supply chain didn’t just get disrupted — it fractured at multiple nodes simultaneously.

What Prediction Markets Actually Priced

Polymarket moved fast on the conflict itself. The US/Israel strike timing market absorbed $529 million in volume. One account (“Magamyman”) netted $553,000 betting on Khamenei’s removal. The platform now hosts 220+ active Iran markets and 109+ Strait of Hormuz contracts, including a “Hormuz closure by March 31” market that resolved at 98% with $28 million in volume, and a “traffic returns to normal by April 30” contract currently at 55%.

But prediction markets have a structural blind spot: they price discrete events, not cascading supply chain consequences. There’s no Polymarket contract for “urea exceeds $700/ton by April.” There’s no Kalshi market on “US corn acres decline 5%+ due to fertilizer costs.” The second-order and third-order effects — the ones that actually reshape the real economy — remain unpriced on these platforms.

That’s where agents win.

The Agent Playbook: Five Steps to the Fertilizer Trade

Here’s the exact pipeline an autonomous agent using the AgentBets four-layer stack would run.

Step 1: Geopolitical Signal Ingestion (Layer 4 — Intelligence)

The agent monitors a feed of geopolitical indicators using CrewAI multi-agent orchestration. One sub-agent tracks US military deployment patterns. Another monitors maritime insurance premiums in the Persian Gulf — these spiked days before the February 28 strikes. A third watches congressional activity and defense contractor stock movements.

The key signal wasn’t the strike itself. It was the insurance premium data. Lloyd’s of London war risk premiums for Hormuz transit began climbing in mid-February. That’s a quantifiable, API-accessible signal that a Claude-powered analysis agent can ingest and weight.

SIGNAL CHAIN (pre-strike):

├── Lloyd's war risk premium: +340% (Feb 15-27)

├── US carrier group repositioning: confirmed via OSINT

├── Polymarket "US strikes Iran" contract: 3% → rising

├── Congressional classified briefing frequency: +2x baseline

└── AGENT ASSESSMENT: P(Hormuz disruption | strike) = 0.82

Step 2: Supply Chain Dependency Mapping (Layer 4 — Intelligence)

This is the step human traders missed — or at least priced with a multi-day lag.

The agent maintains a dependency graph of global commodity supply chains. For fertilizer, the graph looks like:

STRAIT OF HORMUZ DEPENDENCY GRAPH:

├── Natural Gas (feedstock)

│ ├── Qatar LNG → 2nd largest global exporter

│ ├── Iran natural gas → domestic + export

│ └── Impact: ammonia production cost +40-60%

├── Urea (nitrogen fertilizer)

│ ├── Iran: 2nd largest global exporter

│ ├── Qatar: major exporter (halted production)

│ ├── Saudi Arabia: routed through Hormuz

│ └── 50% of global seaborne urea from Persian Gulf

├── Phosphates (DAP/MAP)

│ └── Major Gulf exporters cut off

├── Sulphur

│ └── ~50% of global exports through Hormuz

└── DOWNSTREAM:

├── Corn (35% input cost = fertilizer) → price ↑

├── Wheat (35% input cost = fertilizer) → price ↑

├── Soybean acreage → substitution effect ↑

└── Global food prices → 3-6 month lag

A Polyseer-style Bayesian analysis agent quantifies each node: given Hormuz closure probability of 0.82, what’s the expected urea price impact? Historical analog: the 2022 Russia-Ukraine crisis sent urea to $925/ton. The current disruption affects a comparable share of global supply.

Step 3: Cross-Market Correlation (Layer 3 — Trading)

The agent queries multiple data sources simultaneously through the Polymarket CLOB API and traditional commodity feeds:

| Market | Signal | Timestamp | Agent Action |

|---|---|---|---|

| Polymarket: Hormuz closure | 98% YES | Feb 28 + 4hrs | Confirm disruption |

| Polymarket: Ceasefire by March 31 | ~15% YES | Mar 1 | Confirm duration |

| CBOT Urea futures | $520 → $550 | Mar 3 | BUY (pre-spike) |

| CBOT Wheat futures | +1.2% | Mar 3 | BUY |

| CBOT Corn May ‘26 | $4.57 | Mar 3 | BUY (hit $4.80 by Mar 9) |

| CBOT Soybean futures | +2.1% | Mar 3 | BUY (substitution play) |

| Polymarket: Hormuz normal by Apr 30 | 55% YES | Mar 10 | Inform exit timing |

The critical insight: by March 3, prediction markets had priced the geopolitical event (Hormuz closure at 98%), but commodity markets were still adjusting. Urea had moved from $475 to $520-550 — significant, but not yet reflecting the full disruption math. The North America fertilizer price index didn’t peak at $810 until March 9. That’s a six-day window of alpha.

Step 4: Position Sizing and Execution (Layer 2 — Wallet)

The agent uses a Coinbase Agentic Wallet with pre-set guardrails:

- Maximum position size: 5% of portfolio per correlated trade

- Stop-loss: -15% on any single position

- Correlation limit: No more than 20% exposure to Hormuz-dependent trades combined

- Execution: Split orders across venues to minimize slippage

For the Polymarket leg, the agent places USDC-denominated orders through the CLOB API. For commodity futures, it routes through a traditional brokerage API. The wallet layer handles both crypto and fiat settlement autonomously.

Step 5: Exit Strategy Calibrated to Prediction Markets

This is where the agent loop closes. The Polymarket “Hormuz traffic returns to normal by April 30” contract at 55% YES tells the agent that the market expects resolution is uncertain within the ~7-week window. The “US x Iran ceasefire” market ($19.2M volume) provides a complementary exit signal.

The agent doesn’t need to predict when the war ends. It just needs to monitor the prediction market probabilities and unwind commodity positions as ceasefire probability rises. If ceasefire odds jump from 15% to 50%, the fertilizer supply chain normalizes on a 30-60 day lag — that’s the exit window for agricultural futures.

The Trade That Prediction Markets Can’t Make

This is the fundamental thesis for agent-powered trading: prediction markets excel at pricing binary events but fail at pricing cascading supply chain effects. The fertilizer crisis is a textbook second-order trade.

A human trader on Polymarket could bet on Hormuz closure. A handful did. But connecting “Hormuz closed at 98%” to “buy May corn futures because urea-to-corn ratios will force acreage shifts” requires:

- A maintained supply chain dependency graph

- Real-time ingestion of multiple market feeds

- Historical analog matching (2022 Russia-Ukraine fertilizer crisis)

- Cross-platform execution (prediction markets + commodity futures)

- Autonomous position management over days to weeks

That’s not a human workflow. That’s an agent workflow.

What This Means for Builders

The fertilizer crisis is a template. Every major geopolitical disruption produces second-order and third-order trades that prediction markets don’t cover and human traders are slow to execute. An agent that maps supply chain dependencies — energy → fertilizer → agriculture → food prices — and monitors prediction market probabilities for exit signals has a structural edge.

If you’re building in this space, the stack is clear:

- Identity: Moltbook for persistent agent reputation across platforms

- Wallet: Coinbase Agentic Wallets for cross-venue settlement with spending guardrails

- Trading: Polymarket CLOB for geopolitical signal extraction + traditional commodity APIs for execution

- Intelligence: CrewAI for multi-agent analysis, Claude for reasoning over dependency graphs, Polyseer for Bayesian probability updating

The first agent that ships this pipeline doesn’t need insider information. It just needs the dependency graph, the prediction market feed, and the discipline to trade the second-order effect before the Bloomberg headline lands.

Sources: PBS News, CNBC, Farm Progress, Foreign Policy, The Western Producer, High Plains Journal, Bloomberg, Polymarket, Euronews